Tax rate

What is the general tax rate?

In general, the real estate transfer tax amounts to 3.5 per cent of the tax base. This applies in particular to acquisition processes in return for payment or to the paid share in processes with partial payment, provided that these processes are not taking place within a family unit pursuant to the first line of section 26a paragraph 1 (1) of the GGG. This applies to real estate properties and to agricultural and forestry land.

Caution

These rules also apply to all citizens and entrepreneurs from EU Member States in Austria.

It must be noted here that certain real estate transfers for consideration are treated as acquisition processes without payment and therefore are not subject to the general tax rate.

What is the graduated tariff and when is it used?

The graduated tariff is used

- for acquisitions without payment and for acquisitions considered to be without payment

- acquisitions with partial payment in relation to the unpaid share.

Regarding agricultural and forestry land, this applies only to acquisitions without payment and acquisition processes with partial payment in relation to the unpaid share, which take place outside the family unit pursuant to section 26a paragraph 1 of the GGG.

The tax amounts to

| for the first 250,000 Euro | 0.5 per cent |

| for the next 150,000 Euro | 2 per cent |

| and thereinafter | 3.5 per cent |

of the property value.

Acquisition process without payment

Under the following conditions, the acquisition process is without payment or is considered to be without payment:

- consideration is not provided or is no more than 30 per cent of the property value

- acquisition as a result of death (e.g. inheritance)

- acquisition from a living person within the family unit within the meaning of the first line of section 26a paragraph 1 (1) of the GGG

- Change of shareholder, consolidation or transfer of shares and restructuring within the meaning of the Umgründungssteuergesetz (UmgrStG).

Acquisition process with partial payment

An acquisition with partial payment takes place when consideration amounts to more than 30 per cent but no more than 70 per cent of the property value. The graduated tariff is used for the unpaid share, and the ‘normal tariff’ of 3.5 per cent is used for the paid share.

Where consideration has been given, but cannot be identified

Where consideration has been provided but the amount thereof cannot be determined, the acquisition process is considered to be with partial payment, with consideration of 50 per cent of the property value being assumed. This means that the graduated tariff is applied to half the property value, and the normal tariff of 3.5 per cent is applied to the other half.

When should acquisition processes be aggregated?

To determine the real estate transfer tax according to the graduated tariff, all acquisitions without payment or unpaid share of acquisitions with partial payment from the same person to the acquirer within the last five years are added together (vertically). Aggregation within the five-year period also takes place if the acquirer acquires an economic unit from two or more persons at the same time or successively (horizontal).

All property values of the acquired properties must be added together for the acquirer. The graduated tariff is to be applied once to this total amount. Each acquirer is entitled to the graduated tariff once in full.

Aggregation also takes place if the acquisitions are made at the same time (e.g. with a deed of donation). If several acquisitions are made at the same time, the tax debtor must state the order in which they are to be recorded as prior acquisitions in the tax return or self-calculation. This is particularly important if several transferors are involved whose tax liability depends on the order in which they are added together.

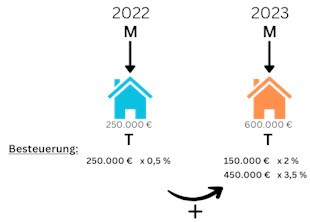

Example

In 2022, daughter T receives a property with a land value of 250,000 Euro as a gift from her mother M. In 2023, T receives another property from M with a land value of 600,000 Euro. There is a case of vertical aggregation between T and M (= several acquisitions between the same persons). As T used up the first tariff level (0.5 per cent) in 2022, 150,000 Euro of the 2023 acquisition fall into the second tariff level (2 per cent) and the remaining 450,000 Euro into the third tariff level (3.5 per cent).

It should be noted that the previous acquisition is not taxed again, but only the tax rate level in the graduated tariff for the last acquisition transaction is higher.

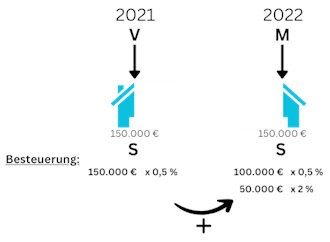

Example

In 2021, son S receives half of a property with a land value of 150,000 Euro from his father. In 2022, S receives the other half of the property from his mother M.

There is a horizontal aggregation (= with regard to the same economic unit). The tax for the two acquisition transactions (half from father to son and half from mother to son) is calculated as if the son had received the property without payment from only one parent. The first half of the property therefore falls entirely into the first tariff level (0.5 per cent), the second half of the property falls into the first tariff level (0.5 per cent) for 100,000 Euro and into the second tariff level (2 per cent) for 50,000 Euro.

What is the procedure for agricultural and forestry land?

In the following acquisition processes of agricultural and forestry land, the real estate transfer tax is 2 per cent of the tax base (which is the simple unit value):

- for acquisitions from living persons in the family unit within the meaning of the first line of section 26a paragraph 1 (1) of the GGG.

- for acquisitions as a result of death (e.g. inheritance) in the family unit within the meaning of the first line of section 26a paragraph 1 (1) of the GGG.

Are there any other tax rates?

For certain acquisition processes (change of shareholder in business partnerships, consolidation or transfer of shares in business partnerships and capital companies) and for processes under the Umgründungssteuergesetz, the tax rate is 0.5 per cent, if the tax is not to be calculated from the unit value (thus does not apply to agricultural and forestry land, the tax rate here is 3.5 per cent).

For the acquisition of property through a private-law foundations or comparable assets, the tax rate increases to 2.5 per cent of the difference between the property value and any consideration (foundation income tax equivalent).

Responsible for the content: Federal Ministry of Finance